The IRS has provided guidance for income tax returns due on April 15. The due date is extended until July 15 for individual, corporation, trust and estate income tax returns. The payment date is also extended for these returns. Any payments deferred until July 15 will not be subject to any interest and penalty charges. This rule also applies to the 4/15 quarterly estimated tax payment. If you cannot file your 2019 income tax return by July 15, 2020, then you can file an extension by July 15, 2020 and pay any amount due at that time. If you owe any money after July 15, 2020, then interest and penalties will apply after that date.

The IRS addressed the following questions:

- The second quarter that is due June 15, 2020 hasn’t been extended to July 15, 2020.

- Gift and estate tax returns haven’t been extended to July 15, 2020.

- Any claim for refunds for 2016 haven’t been extended.

- Forms 706, Estate Tax Returns have due dates that are contingent upon the death of the taxpayer. The IRS Guidance issued does not any extend these returns or returns with extended due dates.

- The change in the filing dates and payment dates are not applicable to fiscal C Corp returns or 990s due May 15 or June 15.

Unfortunately, the IRS has not yet addressed:

- Information returns such as FBARs have also not yet been addressed. Therefore the FBAR apparently is still due April 15 but practically is automatically extended till Oct 15.

- 5500-EZ returns are normally due July 31. Typically, if the underlying 1040 is extended, the 5500-EZ due date is similarly extended till Oct 15. Absent any guidance, an extension for form 5500-EZ may need to be filed before July 31, 2020.

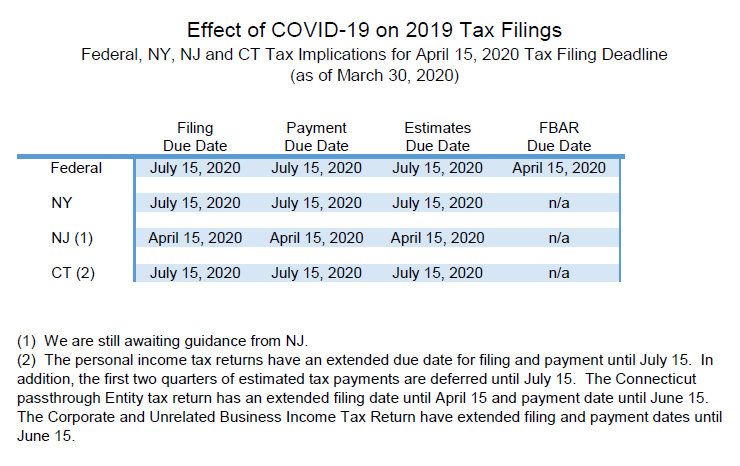

The States have not been uniform in their approach as shown in the grid below.

We will be updating this memo as the IRS and the States provide additional guidance.